Intrexon offered its common equity shares to the public in 2013 making it the first pure synthetic biology company to IPO. I wrote about the company in 2014.

In its IPO disclosures, Intrexon said, “We believe we are the first company focused exclusively on applying synthetic biology across a broad spectrum of end markets and have been working in the field since 1998. Over the last 15 years, we have accumulated extensive knowledge and experience in the design, modification and regulation of gene programs. We believe all of these factors, coupled with our suite of proprietary and complementary technologies, provide us with a first-mover advantage in synthetic biology.” It even had a designer domain name, DNA.COM, to go along with its bespoke ambitions.

Some of the world’s most astute investors heaped praise on the company for its promise to harness synthetic biology’s potential. Third Point’s Dan Loeb said, “We believe that Intrexon is an innovation leader in synthetic biology with a unique value proposition and proven leadership team. Most attractive to us is Intrexon’s potential to transform multiple industries, including the health, food, and energy markets.” And famed investor Bill Miller offered an accompanying perspective with the declaration that the company is, “the stock of the decade.”

Here is Bill Miller’s CNBC interview from 2016:

Business Model

To leverage its synthetic biology technology with collaborators, Intrexon developed a unique business model that centered on Exclusive Channel Collaborations (ECCs) with partners. In exchange for providing access to their technology, Intrexon was to receive cost reimbursement (thus mitigating the need to raise additional external funds) and significant downstream economics. Because Intrexon’s technology is scalable, its capacity to sign ECCs across multiple industries was considered to be limited only by the ambition of its partners. Indeed, as of 2014, Intrexon had already signed over 15 ECCs including with Johnson & Johnson. Intrexon intended to sign multiple ECCs, creating a broad pipeline of projects while diversifying away from specific product risk.

There was a dizzying pace of product development and deal making, creating excess that bulged out of every frame. There was a licensing agreement with the MD Anderson Cancer Center and the University of Minnesota to gain access to the, “most well-defined nonviral gene insertion technology for oncology-related immunotherapeutics.” Intrexon bought out minority investors in Exemplar Genetics, thereby securing full ownership of a subsidiary of Trans Ova Genetics that specialized in large animal models of human diseases. The ActoGenix purchase was intended to broaden Intrexon’s expertise in cell therapies to include medicinal probiotics. Intrexon Energy Partners (IEP) secured a joint venture with $75 million in partner money required to build a pilot plant for the bioconversion of methane to isobutanol.

The company’s Oxitec subsidiary was the first project to draw fire for its controversial ability to control wild populations of disease-carrying mosquitoes in Brazil without the need to spray insecticides. The concept was to release a strain of genetically-modified (GM) mosquitoes that should have only reduced population size and not affected the genetics of the target (native) populations through the engineered inability for lab organisms to mate with their wild counterpart. There were problems and delays: some offspring of the GM mosquitoes survived and produced offspring that also made it to sexual maturity. As a result, local mosquitoes inherited pieces of the genomes of the GM mosquitoes.

Finally, Intrexon’s collection of gene regulatory elements as “switchable” cytokines were considered promising but not easy to engineer. Intrexon negotiated an ECC to test one of its switches in peripheral blood leukocytes (PBL) and a deal with Merck Serono to cover the development of CAR-T cells designed to attach tumors based on novel targets.

Intrexon was led by Chairman and CEO Randal J. Kirk, one of the most successful healthcare leaders at the time. Kirk founded and led New River Pharmaceuticals until its acquisition by Shire, and led Clinical Data through the successful development and approval of the anti-depressant Viibryd before selling the company to Forest. He was personally invested significantly in Intrexon’s success through Third Security, which owned nearly two-thirds of Intrexon’s shares outstanding. Forbes ran a glowing story about Kirk’s $1.5 billion “pop” upon Intrexon’s IPO.

The Aftermath

Between 2014 and 2015, the company’s value swelled from $2 billion to more than $4 billion. But by 2018, Intrexon’s ECCs had not yielded any blockbuster products. For the quarter ended September 30, 2018, total revenues decreased by $9.4 million, and collaboration and licensing revenues decreased sequentially by $8.1 million, or 57%. Research and develop costs rose relentlessly. Cash became a problem. There were numerous secondary offerings of various kinds. For example, in June 2018, Intrexon raised $200.0 million through the issuance of 3.50% convertible senior notes due 2023.

Intrexon was too early, and the company’s dealmakings pace was more about hubris than diversification. Fictive imaginings of whole industries upended by some CRISPR magic gave way to a new reality that the subplots of mini industrial revolutions eventually got excised at gravity’s altar. For example, the hype over $100 per barrel oil price deflated by 2016 when the price of crude had fallen to less than $40 a barrel and obliterated the business case for alternative fuel production.

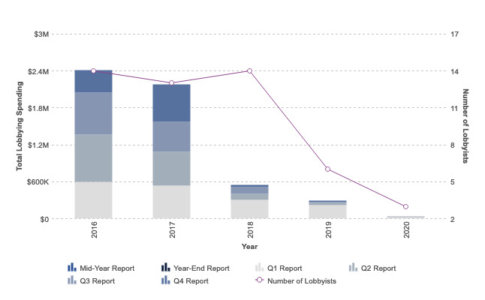

The arc of the synthetic biology story went a different way. CRISPR-Cas9 emerged as a more advanced editing method that delivers fewer off-target edits and greater targeting scope. And as the COVID crisis has reinforced, much of the R&D conducted in the U.S. is funded by the government, and this is especially true for new drug development that is supported by the National Institutes of Health (NIH) and other federal agencies. Intrexon’s meager lobbying efforts make clear that it failed to understand how to convert campaign contributions into free R&D – and ultimately into marketable products protected by patent moats and by required U.S. government buying.

The company changed its name to Precigen in 2020.

Here’s what happened with the competition:

Craig Venter’s company Synthetic Genomics concluded a long-term deal with ExxonMobil to develop algae biofuel. The team identified the genetic switch for producing oil in the algae species Nannochloropsis gaditana. It then modified it to produce oil under adverse conditions. The result, reported in the journal Nature Biotechnology in June 2017, was a doubling of the algae’s oil content – from 20% to more than 40% – with no significant impact on the algae’s growth. ExxonMobil anticipates that 10,000 barrels of algae biofuel per day could be produced by 2025 based on research conducted to date and emerging technical capability.

According to MIT News, researchers at MIT developed a synthetic gene circuit by triggering the body’s own immune system. The circuit only activates a therapeutic response when it detects two specific cancer markers. “There has been a lot of clinical data recently suggesting that if you can stimulate the immune system in the right way you can get it to recognize cancer,” says Timothy Lu, associate professor of biological engineering and of electrical engineering and computer science at MIT and head of the Synthetic Biology Group in MIT’s Research Laboratory of Electronics. “Some of the best examples of this are what are called checkpoint inhibitors, where essentially cancers put up stop signs [that prevent] T-cells from killing them. There are antibodies that have been developed now that basically block those inhibitory signals and allow the immune system to act against the cancers.”

At the J. Craig Venter Institute, Drs. Yo Suzuki and John Glass have created a synthetic version of beta cells (the cells that produce and release insulin) in 2019. Dr. Suzuki was awarded funding from the Diabetes Research Connection to explore converting a naturally residing deep skin bacterium into a surrogate beta cell. This pilot project was successful. The results suggested that the skin bacterial cells could be engineered to respond to blood glucose levels and produce insulin. The team is expanding on this research to see if the synthetic beta cells function robustly in additional tests and thus could be developed as a future alternative to injected insulin.

The market’s merciless eye for weakness took its last bite on Thursday, January 2, 2020, when Randal J. (RJ) Kirk resigned as Chief Executive Officer of Intrexon after almost 11 years in the role.