The stock market is designed to appraise the commercial, not the scientific, potential of new medicines. Clinical progression is the only real measure of an early-stage biotech’s commercial potential. Sometimes clinical trial design can cloud the picture of a promising drug candidate – where flaws in read-outs may not be indicative of true value. And the same is true in reverse.

Here are three speculative biotechs in Phase 2 and Phase 3 that can be characterized as having a lot of asymmetry in terms of risk/reward. One component of this risk/reward is the practical reality that a firm’s size impacts liquidity and availability to professional managers, creating an air pocket through which market caps can plummet due to market cap size. Whether it is due to size or trial design, the potential for mispricing is much higher with smaller biotechs.

This is not a recommendation. These ideas are only for speculative investors. Risk of total loss is high. If the investment challenge were a problem of general statistics (passive), a typical investor would flee. There is an alternative point of view that argues for specific odds (active) shaped through the creation of unique knowledge. The following is a description that may be helpful in making an independent appraisal of specific situations.

Market Cap: $3 million

Cash: Very low

IP: Extensive

Major clinical progression: In Phase 3 w/o significant AEs

Major Indications: Glioblastoma (adult) & diffuse midline gliomas (DMG), including diffuse intrinsic pontine gliomas (DIPG) in childhood brain cancer with poor prognosis and limited treatment options

Readout: expected by June 30, 2024

NIH, National Cancer Institute: Link To Clinical Trials

Personal Interview: CEO via Zoom in May 2024

Market Cap: $490 million

Cash: $350 million

IP: Extensive

Major clinical progression: Two drugs in Phase 3 w/o significant AEs

Major Indications: Diabetes Type 2 Chronic Kidney Disease – End-Stage Renal Failure

Readout: expected by June 30, 2024

Link to Clinical Trials

Personal Interview: Chief Business Officer via Zoom in March 2024

Market Cap: $50 million

Cash: $87 million as of December 31, 2023

IP: Extensive

Major clinical progression: Two drugs in Phase 1/2a with modest AE

Major Indications: Cancer

Readout: Year End 2024

Link to Clinical Trials

Personal Interview: CEO via Zoom in May 2024

KAZIA

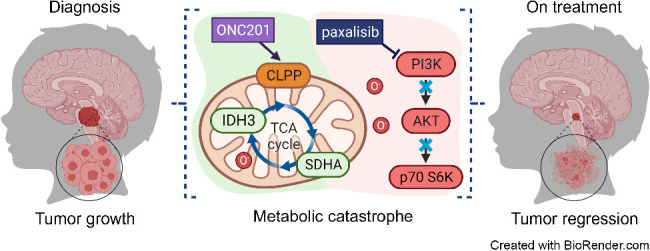

KZIA’s lead program is paxalisib (formerly known as GDC-0084), a small-molecule dual inhibitor of the phosphatidylinositide 3-kinase (PI3K) pathway and the mammalian target of rapamycin (mTOR), which was licensed from Genentech, Inc. in October 2016. Paxalisib is different from the majority of molecules in this class due to its ability to cross to the blood-brain barrier, which has been demonstrated in multiple animal species and confirmed in human data. The drug is protected by granted or pending composition-of-matter patents in all commercially relevant territories. Loss of exclusivity varies between territories but is no earlier than 2030 in any territory.

Paxalisib was granted Orphan Drug Designation (ODD) for glioblastoma by the US FDA in February 2018, and for the broader indication of glioma in August 2020. Paxalisib was granted Rare Pediatric Disease Designation (RPDD) for certain forms of childhood brain cancer by the FDA in August 2020 and was also granted Fast Track Designation for glioblastoma in August 2020. In addition, paxalisib was granted ODD by the FDA for the treatment of atypical rhabdoid/teratoid tumours (AT/RT), a rare pediatric brain cancer, in June 2022 and RPDD in July 2022.

Paxalisib in combination with radiation therapy was also granted Fast Track Designation for patients with solid tumor brain metastases and PI3K pathway mutations in July 2023. Collectively, these special designations provide paxalisib with enhanced access to the FDA, a waiver of PDUFA fees, a period of data exclusivity and, in the specific cases of RPDD, the potential to secure a pediatric Priority Review Voucher (pPRV) should paxalisib be approved.

Paxalisib has completed a 47-patient Phase I clinical study under Genentech in patients with progressive or recurrent high grade glioma (NCT01547546), which showed the drug to be generally safe and well-tolerated, and which provided pharmacodynamic proof of concept and signals of potential clinical activity. This study was published in Clinical Cancer Research, and a companion paper detailing a post hoc analysis of imaging data from the study has been published in the same journal. The company has completed a Phase II clinical trial of paxalisib in newly diagnosed glioblastoma patients with unmethylated MGMT promotor status (NCT03522298), which is expected to be the primarily target population at commercial launch. This study has confirmed the safety profile and pharmacokinetic parameters of the drug in this specific population, and has provided convincing signals of clinical efficacy. Final data from the completed Phase ll study of paxalisib was presented at several neuro-oncology and medical oncology conferences. The key findings included a median overall survival of 15.7 months, which compares favorably to the figure of 12.7 months that has been reported for temolozolomide, the existing standard of care.

In October 2020, KZIA executed a definitive agreement with the Global Coalition for Adaptive Research (GCAR) to introduce paxalisib into the ongoing adaptive platform study, GBM AGILE (NCT03970447). This study is designed to provide substantial evidence for approval of new drugs in glioblastoma, and is intended to serve as the pivotal study for paxalisib in US, EU, and other markets. The first patient recruited by a site opened to the paxalisib arm occurred in January 2021. In November 2021, the study opened to recruitment in Canada. Expansion to several countries in Europe was completed during CY2022. Final data from the GBM AGILE study is anticipated during 1H CY2024.

The most recent cause for doubt about the company’s future occurred in August 2022 when KZIA announced that it had been informed by GCAR that the paxalisib arm had not graduated to the second stage of the GBM AGILE study, and that recruitment had therefore completed with approximately 150 patients enrolled to the first stage. Those patients remain ongoing, with final data anticipated by June 30, 2024. KZIA says interim ‘graduation’ analysis may have been affected by the rapid and back-loaded recruitment profile of the study and does not preclude a positive outcome in the final data.

Eight investigator-initiated studies continued to progress during the period: a phase ll study in DIPG and other diffuse midline pediatric gliomas run by the Pacific Pediatric Neuro-Oncology Consortium (PNOC) (NCT05009992), a Phase II study with paxalisib in HER2+ breast cancer brain metastases at Dana-Farber Cancer Institute in Boston, MA (NCT03765983), a Phase II multi-drug, genomically-guided study in brain metastases run by the Alliance for Clinical Trials in Oncology (NCT03994796), a Phase I study with paxalisib in combination with radiotherapy for brain metastases at Memorial Sloan Kettering Cancer Center in New York, NY (NCT04192981), a Phase II study with paxalisib in primary CNS lymphoma at Dana-Farber Cancer Institute in Boston, MA(NCT04906096), a Phase ll study in glioblastoma with ketogenesis run by Weill Cornell Medicine (NCT05183204), a Phase I study in low grade glioma run by University of Sydney (LUMOS2) and a phase I study in children with high grade glioma and PI3K pathway mutations (OPTIMISE).

The investigator-initiated PNOC study is a phase II multi-arm study, which includes several combinations of paxalisib with ONC201 (Chimerix, Inc), in paediatric patients with diffuse midline gliomas, including DIPG (NCT05009992). This study is run by the Pacific Pediatric Neuro-Oncology Consortium (PNOC), based at the University of California, San Francisco. In October 2022, KZIA announced the expansion of the PNOC022 study to Australia and additional sites in Israel, the Netherlands, and Switzerland. Preliminary data was presented at SNO Annual Meeting in Vancouver in November 2023. The overall survival in the first 68 patients enrolled was reported at 16.5 months which compares favorably to historical controls of 8-12 months. In August 2022, KZIA announced the presentation of promising new data from an ongoing phase l study of paxalisib in combination with radiotherapy for the treatment of brain metastases, sponsored by Memorial Sloan Kettering Cancer Center in New York, NY.

Interim data from the first stage of the study was presented during an oral presentation at an international neuro-oncology conference on CNS clinical trials and brain metastases. The data reported in the initial exploratory stage that of the 9 patients evaluated for efficacy, all 9 patients exhibited a clinical response, according to RANO-BM criteria, with breast cancer representing the most common primary tumour. Recruitment to the expansion stage has commenced, with the objective of recruiting up to an additional 12 patients.

KZIA announced in March 2023 that it has entered into a collaboration with the Australian and New Zealand Children’s Haematology / Oncology Group (ANZCHOG) for a phase II clinical study examining paxalisib in children with advanced solid tumours, including brain tumours. The study, OPTIMISE, will combine paxalisib with chemotherapy for children with specific genetic mutations in their tumours. The study will harness expertise and insights gained from the Zero Childhood Cancer Program, which aims to match childhood cancer patients with targeted therapies suited to the unique characteristics of their tumor.

In June 2023, KZIA announced that it is supporting the University of Sydney on a molecularly-guided phase II clinical study to examine paxalisib in adult patients with recurrent/progressive isocitrate dehydrogenase (IDH) mutant grade 2 and 3 glioma (G2/3 gliomas). The first patient was enrolled and dosed on the paxalisib arm in 4Q23.

In the context of a previously declared strategy to explore the use of paxalisib in cancers outside the central nervous system, KZIA has entered into a number of research collaborations with leading cancer centers. In October 2022, such a collaboration at the Huntsman Cancer Center at the University of Utah presented preclinical data for paxalisib in melanoma at a conference for melanoma research in Edinburgh, Scotland.

The data, summarized in a poster presentation, demonstrated potent single agent activity for paxalisib, as well as synergy with BRAF and MEK inhibitors, which are standard of care therapies in this disease. In November 2023, this data was published in the high impact journal, Molecular Cancer Therapeutics. In December 2022, KZIA announced a research collaboration with the Queensland Institute of Medical Research, to explore the use of paxalisib as an immodulator in the treatment of solid tumors. This work potentially identifies a novel mechanism of action for the drug, and consequently has been patented to secure novel intellectual property. Potentially, the project may support use of the drug in combination with immuno-oncology therapies.

KZIAs second R&D program is EVT801, a small-molecule selective inhibitor of vascular endothelial growth factor receptor 3 (VEGFR3), which was licensed from Evotec SE in April 2021. The development candidate exhibits a very high degree of selectivity for VEGFR3 over other protein kinases, and this is expected to be associated with a favorable toxicity profile in the clinic and, potentially, a lesser propensity for secondary resistance. In December 2022, scientists working for and with Evotec SE published a summary of their preclinical research on the drug in the cancer journal, Cancer Research Communications. The paper outlines the substantial body of evidence supporting the activity of EVT801 as an anti-cancer therapy, and includes comparative data against several approved therapies with similar mechanisms of action. The paper also presents combination data with several immuno-oncology agents showing evidence of synergy.

A phase I multiple-ascending dose study of EVT801 in patients with advanced cancer (NCT05114668) is ongoing. This study is designed to provide information on the safety, tolerability, and pharmacokinetics of EVT801 in humans, and to establish the maximum tolerated dose for future studies. The study also includes a rich suite of translational biomarkers which will provide detailed information about the pharmacological activity of the drug. The study is ongoing at two sites in France, with clinical data anticipated in CY2024.

KZIA Recent Events

On 8 January, 2024, KZIA received notice from Karen Krumeich of her intention to resign as the KZIA’s Chief Financial Officer, effective immediately.

On 11 January, 2024, KZIA’s Board of Directors appointed Gabrielle Heaton as its Principal Accounting Officer and Principal Financial Officer, effective 15 January, 2024.

On 18 January 2024, KZIA announced the appointment of pharma industry executive, Mr. Robert Apple to Kazia’s Board of the Directors as a Non-Executive Director.

During the month of February 2024, KZIAraised total proceeds for the period of US$447,788 (A$685,280) using the ATM facility and continues to seek additional funding sources both in Australia and overseas.

On 21 February 2024, Armistice Capital exercised 1,824,445 prefunded warrants for a cash price of US$18,244 and 18,244,450 ordinary shares were issued.

PROKIDNEY

I met with Nikhil Pereira-Kamath, Chief Business Officer, another of ProKidney’s recent hires, in March 2024 via Zoom to get a sense of where things stand. I have previously described PROK as a compelling biotech developing novel cell therapies to treat late stage CKD, and, in particular, ESRD, under a wide range of commercial scenarios – where cell therapies are unproven in CKD, and there are no other viable treatment options. The “wide range of scenarios” has delivered in terms of clouding the picture of PROK’s target profile and proof of mechanism for React (rilparencel), the company’s autologous cell therapy. Also, the company has made a number of senior management changes. In summary, PROK appears to be on track in terms of Phase 2 & pivotal Phase 3 clinical progression, with key readouts coming mid-year 2024 and 2025 that will clarify the protocol update (towards patients with highest risk of kidney failure) and include results from bilateral dosing which could improve treatment effect and which could be a financeable catalyst in the next 12 months. I expect new leadership to assert a timeline for drug approval in 2027. Given the company’s depressed valuation, down about 90% in recent months (trading at or below cash of ~$350m), the risk/reward looks compelling in the context of a portfolio of small cap biotechs. Here are the issues as I see them:

- Chamath Palihapitiya. Chamath’s violent exit as a key shareholder of the company culminated in the company repurchasing most of his shares. On November 19, 2023, ProKidney Corp entered into a share repurchase agreement with SC Pipe Holdings LLC and SC Master Holdings, LLC, pursuant to which the Company agreed to repurchase an aggregate of its 7,256,367 Class A ordinary shares for $1.309 per share. According to the latest Form 4 filing, Chamath still holds 3m shares held by a trust for the benefit of his immediate family, after this repurchase… but outside of this family trust (which LifeSci, the company’s IR firm, has confirmed cannot be touched), he no longer owns shares.

- GLP-1. The GLP-1 agonist weight loss bandwagon appears to have subsided at least in terms of the new class of drug’s potential impact on CKD any time soon. For example, DaVita’s stock has recovered dramatically, nearly doubling since the low in September 2023, presently trading near a 10-year high.

- Changes to one of the company’s clinical programs. PROK has made changes to its Phase 3 development program to exclude Stage 3a patients and focus on patients with Stage 3b and 4 diabetic CKD, who are at the highest risk of advancing to kidney failure and requiring dialysis. This includes modifying the eGFR enrollment range for the proact 1 Phase 3 clinical study to align with the results and feedback from the RMCL-002 study. This will delay enrollment until the first half of 2024. However, the eGFR enrollment range for the second Phase 3 trial, proact 2 (REGEN-016), will remain unchanged to enable the company to seek a broader commercial label.

- Delay in manufacturing. The company has temporarily paused manufacturing to address deficiencies in the documentation of quality management systems identified during a recent audit. The company aims to optimize its capabilities to meet EU and global standards for its Phase 3 program and future commercial manufacturing, with plans to resume manufacturing in the first half of 2024. No safety issues are involved in this delay, according to the company.

- What is the impact on TAM? Here I have collected the pieces that make up a DCF model and will leave the final analysis until clarifying readouts are available later in 2024 and 2025. In summary, the parts suggest a novel product with peak sales in the billions annually for a disease state with no other therapy options. First, I observed one change in messaging. Previously, the company and the Street hoped for the potential for reparative/regenerative capability to drive more robust disease modifying activity vs SOC. Today, the company is messaging around stabilization and delay of onset of ESRD. 10-K 2023: “Clinical studies suggest that REACT can impact kidney function positively by stabilizing eGFR, or attenuating the rate of eGFR decline, in patients with CKD caused by type 2 diabetes.” vs S-1 2022: “Our lead product candidate, which we refer to as REACT, is designed to stabilize or improve kidney function in a CKD patient’s diseased kidneys.” Again, I believe this is a messaging issue, and the team will rely on clinical results to show improvement if any are demonstrated. Any such improvement would be a surprising additional benefit. TAM data: Based on available U.S. data from the 2018 National Health and Nutritional Examination Survey, the company expects the aggregate CKD population in the US and EU to grow from approximately 70 million in 2020 to approximately 80 million in 2030 and approximately 93 million in 2040. The most common causes of CKD among adults are diabetes, hypertension, and glomerular disease, and in the pediatric population, CAKUT. In the US, it is believed that approximately 3.2 million patients per year suffer from stage 3b or 4 CKD, and 1.2 to 1.8 million of those patients could be eligible for treatment with rilparencel. More than 135,000 of these CKD patients progress to dialysis every year. Total annual costs to Medicare for patients with CKD (including ESRD) exceed $138B. Dialysis treatment costs Medicare about $100k per year with survival rate of about five years. Private payors can pay orders of magnitude more than Medicare. A report by Bank America (2022) suggested pricing of $360k for once-and-done treatment based on an extrapolation of recent non-CKD specialty drug launch pricing.

- Variables include: Potential label expansion to re-dose rilparencel for longterm dialysis prevention, clinical evidence of potential to reverse progression of kidney disease in CKD patients, timing of additional readouts, timeline for drug approval, durability as measured by a parallel control group in Phase 3, in which case there may be a need for re-dosing in 18- to 24-months.

- I have only heard the new CEO, Bruce Culleton MD, speak in the November 2023 conference when he was introduced. Since then, there are two other events listed ProKidney’s website but they contain no content.

IMMUNEERING CORP

IMRX is advancing its clinical programs with a focus on oncology, targeting the MAPK pathway. Their drug development approach emphasizes the cyclical disruption of signaling pathways to balance therapeutic efficacy and minimize toxicity, a method they term “Deep Cyclic Inhibition.”

Their main clinical programs include:

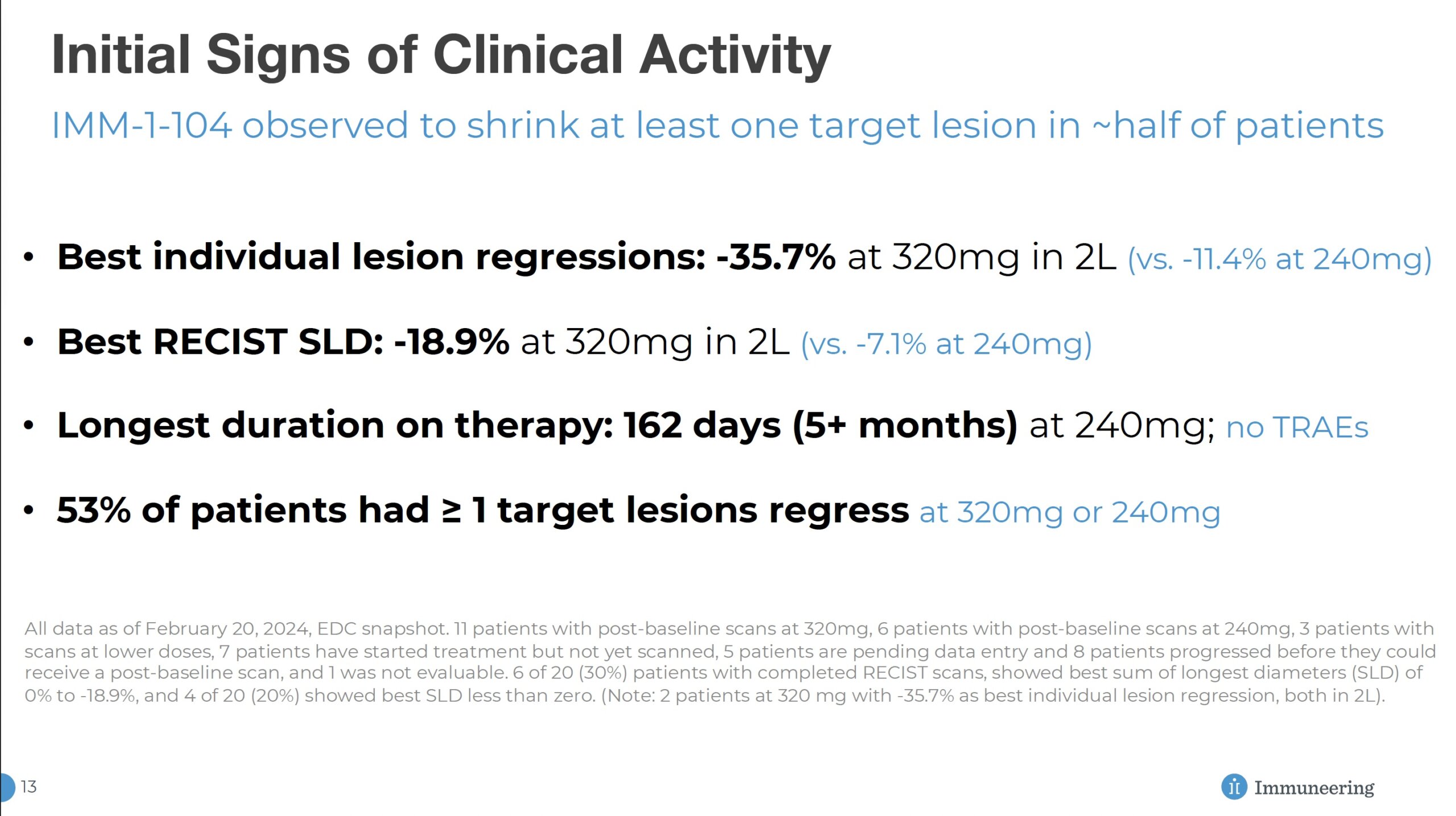

- IMM-1-104: This drug candidate targets universal-RAS activity with once-daily oral dosing. It’s designed to impact cancer cells significantly more than healthy cells by leveraging deep cyclic inhibition of the MAPK pathway. IMM-1-104 is currently in a Phase 1/2a study for patients with advanced solid tumors that harbor RAS mutations.

- IMM-6-415: Another deep cyclic inhibitor, this candidate focuses on both RAS and RAF mutations, administered with a shorter half-life to allow twice-daily dosing. It’s also in a Phase 1/2a trial for advanced solid tumors.

The technology platform at IMRX integrates bioinformatics and computational biology, which helps to streamline the drug development process. This platform is powered by their ability to analyze high-throughput Omics data, including transcriptomics, genomics, and proteomics. This approach allows them to identify unique disease mechanisms and patient subsets, which facilitates the discovery of novel targets and drug candidates with potentially better safety and efficacy profiles

IMRX’s platform also involves a proprietary AI technology named Fluency for rapid screening of small molecules, aiming to optimize the interaction with specific targets. This method is part of their broader strategy to innovate drug chemistry and dynamics to address the challenges of traditional drug development.

The main challenge for the company was a Phase 1 readout in March 2024 that spooked several key investors and created a major downdraft in share price. Management thinks that using 104 earlier in treatment could improve response rates to levels that the market desires. They expect this dimension of clinical design, which is present in phase 2a (currently underway), to lower the emergence of new mutations found in other pathways. According to management, this approach, combined with the challenges of the advanced Phase 1 patient population, was a key factor in the minimal response observed from 104 in Phase 1.

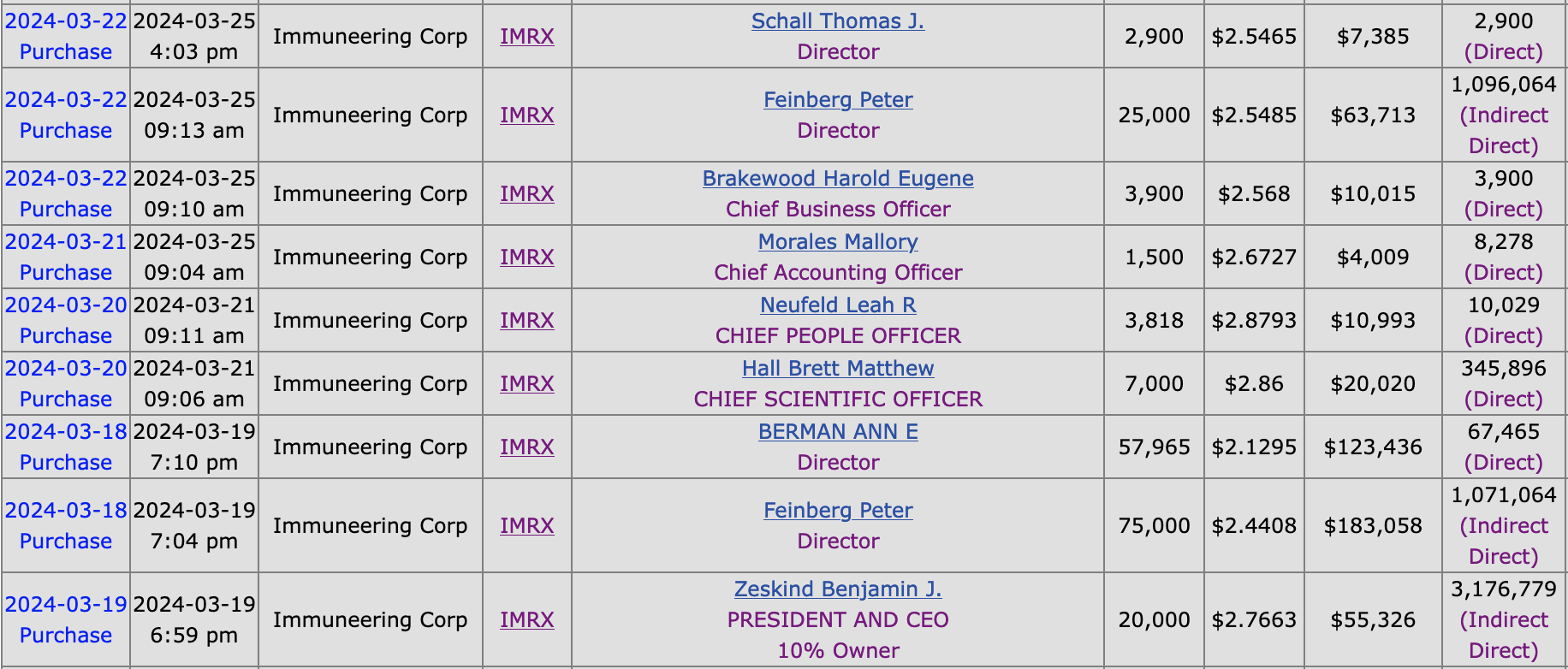

Finally, it is reassuring that insiders took advantage of the recent selloff in the company’s share price.

The ideas presented on this site do not constitute a recommendation to buy or sell any security. Investors are advised to conduct their own independent research into individual stocks before making a purchase decision. In addition, investors are advised that past stock performance is not indicative of future price action. You should be aware of the risks involved in stock investing, and you use the material contained herein at your own risk. Neither SYNTHETIC.COM nor any of its contributors are responsible for any errors or omissions which may have occurred. The analysis, ratings, and/or recommendations made on this site do not provide, imply, or otherwise constitute a guarantee of performance. SYNTHETIC.COM posts may contain financial reports and economic analysis that embody a unique view of trends and opportunities. Accuracy and completeness cannot be guaranteed. Investors should be aware of the risks involved in stock investments and the possibility of financial loss. It should not be assumed that future results will be profitable or will equal past performance, real, indicated or implied. The material on this website is provided for information purpose only. SYNTHETIC.COM does not accept liability for your use of the website. The website is provided on an “as is” and “as available” basis, without any representations, recommendations, warranties or conditions of any kind.